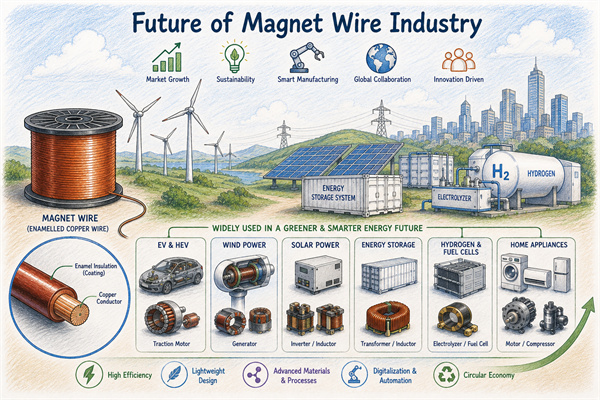

Future of Magnet Wire Industry I. Market Size and Growth Trends

1.1 Overall Market Size

The global magnet wire market size was approximately US$32 billion in 2024. It is projected to grow to US$48-52 billion by 2030 and exceed US$70 billion by 2035. The compound annual growth rate (CAGR) is approximately 6-8%. This growth is driven by two forces: on the one hand, the explosive growth of new energy vehicles, energy storage, and renewable energy has brought new demand; on the other hand, the replacement market for traditional applications (home appliances, industrial motors, transformers) remains stable.

1.2 Market Segment Size

| Application Segment | 2024 Size (USD bn) | 2030 Size (USD bn) | CAGR (%) |

|---|---|---|---|

| Industrial Motors | 95 | 125 | 5.0 |

| Transformers | 75 | 105 | 5.5 |

| Home Appliances | 50 | 60 | 3.0 |

| Electric Vehicles (EV) | 35 | 95 | 18.0 |

| Renewable Energy (Wind + Solar) | 28 | 65 | 15.0 |

| Energy Storage (BESS) | 15 | 55 | 25.0 |

| Others (Aerospace, Medical, 5G) | 22 | 25 | 2.0 |

II. Technological Development Trends

2.1 High Frequency and High Power Density

The rapid popularization of third-generation semiconductors (SiC, GaN) is driving the magnetic wire industry towards higher frequencies. Traditional silicon-based IGBTs operate at frequencies of 10-20 kHz. SiC inverters, on the other hand, can operate at frequencies of 100-500 kHz, and GaN devices can even reach the MHz level. Higher frequencies place new demands on magnetic wires.

The skin effect and proximity effect are significantly amplified at high frequencies, resulting in AC resistance much greater than DC resistance. Litz wire and thin-film insulated wire (FIW) will become the mainstream choices for high-frequency applications. It is projected that by 2030, the global high-frequency magnetic wire market will account for 25-30% of the overall magnetic wire market – a brand new high-value-added sector.

2.2 The voltage levels of renewable energy systems are continuously increasing.

Wind power is rising from 690 V to 1,500 V and 3,300 V, with future offshore wind power reaching 66 kV. Photovoltaics are rising from 1,000 V to 1,500 V and 2,000 V. Energy storage PCS is rising from 1,500 V to 2,000 V and 3,000 V.

This increase in voltage places higher demands on the withstand voltage of magnetic wire enamel coatings. Grade 3 thickened enamel coatings (breakdown voltage ≥ 6,000 V) will gradually replace Grade 2 as the mainstream. Class N 200°C enamel coatings (polyamide-imide AIW/200) will find wider application in high power density applications.

2.3 High Power Density and Miniaturization:

Applications such as EV drive motors, rail traction motors, and aerospace motors are increasingly demanding higher power density. Taking EV drive motors as an example, the typical power density in 2020 was 3-4 kW/kg, reaching 5-6 kW/kg in 2024, and is projected to reach 8-10 kW/kg by 2030.

This means that for the same power output, the size and weight of the motor will continue to decrease—the filling density of the winding wire, the heat resistance of the enamel coating, and the heat dissipation capacity must be improved simultaneously. New winding technologies such as flat wire (rectangular wire), hairpin winding, and continuous wave winding will become the mainstream for high power density motors.

III. Material Innovation Trends

3.1 Accelerated Progress of

Aluminum Substitution for Copper: High copper prices (2024-2026 LME 8,500-10,500 USD/ton) continue to drive the engineering application of aluminum replacing copper. Aluminum wire has historically been primarily used in power distribution transformers and large motors.

After 2025, its application in EVs, home appliances, and industrial motors will rapidly expand. The core drivers for aluminum replacing copper are fourfold: cost (aluminum is about one-third the price of copper), weight (aluminum’s density is 30% of copper’s), strategy (geopolitical risks associated with copper resources), and carbon emissions (aluminum’s carbon emissions are lower than copper’s). It is projected that by 2030, aluminum’s share of the global wire market will increase from 15% in 2024 to 30%.

3.2 Copper-clad

Aluminum (CCA) and Copper-clad Copper (CCC) Copper-clad aluminum (CCA) wire represents a transitional form between copper and aluminum. It combines the surface conductivity of copper with the lightweight and low cost of aluminum, offering advantages in medium-power applications.

Copper-clad copper (CCC) wire uses a copper core and copper plating structure, reducing costs while maintaining conductivity. In 2024, the global CCA/CCC wire market size was approximately $800 million, and it is projected to grow to $2-2.5 billion by 2030, with a CAGR of approximately 16%.

3.3 Innovation in Enamelled Coating Materials Enamelled coating is one of the core technologies of magnet wire.

In the next 5-10 years, innovation in enamel coated materials will mainly focus on the following areas: High temperature resistance: High-temperature enamel coatings such as polyimide (PI), polyamide-imide (PAI), and polyetheretherketone (PEEK) will gradually replace traditional polyester imides.

Low loss: Nano-modified enamel coatings (adding SiO₂ and Al₂O₃ nanoparticles) can reduce high-frequency losses by 15-25%. Environmental friendliness: Solvent-free and water-based enamel coatings will gradually replace traditional solvent-based enamel coatings. Intelligent technologies: Self-healing enamel coatings (incorporating microcapsules) and temperature-sensitive enamel coatings (color changes with temperature) are moving from the laboratory to engineering applications.

IV. Industry Landscape and Supply Chain

4.1 Regional Landscape Changes

In 2024, the global magnetic wire production capacity distribution was roughly as follows: China accounted for 55%, Japan 12%, South Korea 5%, Europe 12%, North America 10%, and other regions 6%.

China will continue to maintain its position as the world’s largest magnetic wire producer in the next 5-10 years—but the growth rate of production capacity will slow down, and technological upgrades will become the main theme. Japan maintains its leading position in the high-end magnetic wire (Class N, AIW/200, special enameled wire) field. Germany (Bedra, Elektrisola) and the United States (Rea, MWS) maintain their advantages in the fields of high-frequency Litz wire and special-purpose magnetic wire.

4.2 Accelerated Industry Consolidation

The magnetic wire industry is undergoing accelerated consolidation. Between 2020 and 2024, the global magnetic wire industry saw over 30 major mergers and acquisitions. The consolidation followed two main directions: horizontal integration—large magnetic wire companies acquiring regional small and medium-sized manufacturers to expand production capacity and market coverage; and vertical integration—magnetic wire companies extending upstream (copper rods, aluminum rods, paint) or downstream (winding processing, motor assembly).

It is projected that by 2030, the market share of the top 10 global magnetic wire suppliers will increase from 45% in 2024 to 60%—significantly increasing industry concentration.

4.3 Supply Chain Diversification

The COVID-19 pandemic, geopolitics, and trade frictions have made the magnetic wire industry realize the importance of supply chain diversification. Tier 1 customers (especially leading companies in EVs, energy storage, and wind power) are beginning to require suppliers to establish a “dual-base + multiple raw material sources” supply system. This means that magnetic wire companies need to establish production bases in 2-3 different regions and ensure that key raw materials (copper rods, aluminum rods, paint) have multiple qualified suppliers.

V. Policy and Compliance Trends

5.1 The Profound Impact of Carbon Tariffs (CBAM)

The EU Carbon Border Adjustment Mechanism (CBAM) will be officially implemented on January 1, 2026, and fully operational by 2030. CBAM requires all imported steel, aluminum, fertilizer, cement, electricity, hydrogen, and other products to declare their carbon footprints. For the wire industry, carbon emissions from copper and aluminum rods will become a new compliance requirement. Wire companies must establish a product carbon footprint accounting system—covering the entire lifecycle of carbon emissions from raw material procurement, manufacturing, logistics, and end products. Wire companies that proactively manage their carbon footprints will gain a competitive advantage in the EU market after 2026.

5.2 Continuous Updates to RoHS 3.0 and REACH RoHS 3.0 (2015/863/EU) includes phthalates (DEHP, BBP, DBP, DIBP) in the restricted substances list.

The REACH regulation continuously updates the Substances of Very High Concern (SVHC) list. In the next 5-10 years, the magnetic wire industry will face stricter chemical compliance requirements—including flame retardants (PFAS restrictions on perfluorinated compounds), heavy metals (lead, cadmium, chromium), and plasticizers.

5.3 Indirect Impact of the US IRA Act

The US Inflation Reduction Act (IRA)’s localization requirements for the EV industry indirectly affect the global supply chain layout of the magnetic wire industry. The IRA stipulates that a certain percentage of “critical minerals” in battery components eligible for tax credits in EVs must originate from the US or countries with free trade agreements. This has led many magnetic wire companies to establish new bases in the US, Mexico, and Canada to serve North American EV customers.

VI. Application Driver Analysis

6.1 New Energy Vehicles:

The Biggest Growth Engine EVs are the biggest growth engine for the magnetic wire industry over the next 10 years. Each EV drive motor uses approximately 5-15 kg of magnetic wire (depending on power rating). Each EV charger uses approximately 1-3 kg of magnetic wire. Each EV on-board charger (OBC) uses approximately 0.5-1 kg of magnetic wire. Global EV sales reached approximately 17 million units in 2024 and are projected to reach 40-45 million units by 2030. This means the EV magnetic wire market size will grow from $3.5 billion in 2024 to $9.5 billion in 2030.

6.2 Energy Storage:

The Second Growth Engine Battery energy storage systems (BESS) are the second largest growth engine in the magnetic wire industry. Global new BESS installations reached approximately 180 GWh in 2024 and are projected to reach 800-1,000 GWh by 2030. The magnetic wire usage per 100 MWh BESS power station is approximately 30-60 tons. The BESS magnetic wire market size is projected to grow from $1.5 billion in 2024 to $5.5 billion in 2030.

6.3 AI Data Centers: An Emerging Growth Engine AI data centers emerged as a new growth engine after 2024.

The power consumption of a single AI server rack jumped from the traditional 5-10 kW to 30-100 kW. Liquid-cooled, high-power-density AI servers created new demands for high-frequency magnetic wire (Litz wire, film-insulated wire). The AI data center magnetic wire market is projected to reach $800-1.2 billion by 2030—a completely new segment. ## VII. Conclusion The future of the magnetic wire industry will be driven by four emerging applications: EVs, energy storage, renewable energy, and AI data centers.

The market size will grow from $32 billion in 2024 to $48-52 billion in 2030 and over $70 billion in 2035. Technological trends towards higher frequencies, higher voltages, higher power densities, and aluminum replacing copper are irreversible directions. In terms of industry structure, China will continue to dominate production capacity, while Japan, Germany, and the United States will maintain their advantages in the high-end magnetic wire sector, and industry consolidation will accelerate.

Regarding policy compliance, CBAM, RoHS 3.0, and the IRA will reshape the global supply chain. For magnetic wire companies: seize the four growth engines of EVs, energy storage, renewable energy, and AI data centers; proactively deploy new technologies such as Class N enamel coating, flat wire, CCA/CCC, and high-frequency Litz wire; establish a product carbon footprint accounting system; and promote supply chain diversification. For magnetic wire users: choosing suppliers with technological upgrade capabilities, production capacity stability, certification completeness, and carbon footprint management capabilities is the foundation of long-term product competitiveness.